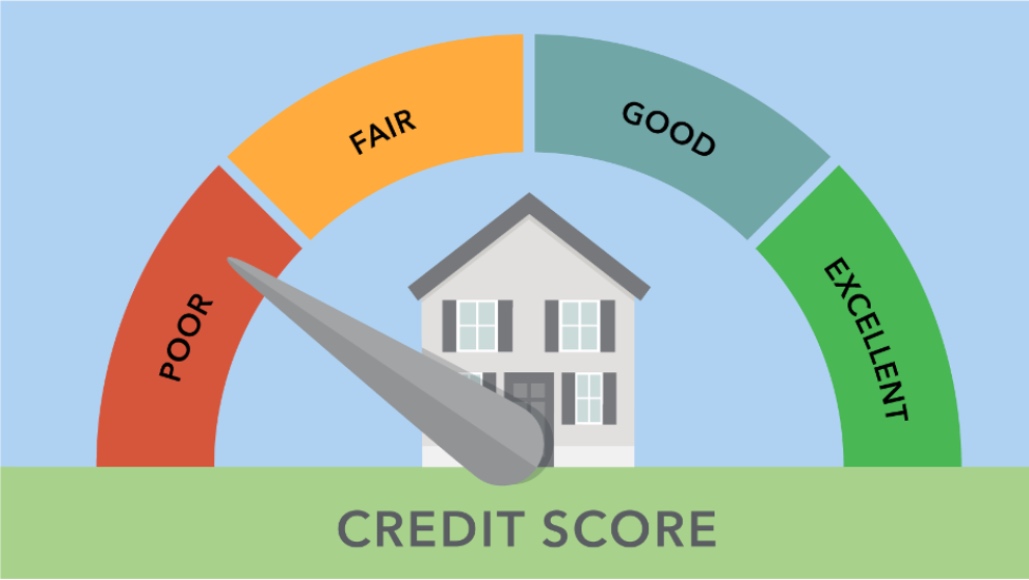

7 signs that show you have a bad credit score

It is vital not to turn a blind eye to your credit report. Even though your business is making you too busy, or you are just full of fear of what you will see concerning your business credit score. Whatever the case, it is best to have an idea of how your credit reports and scores look. Also, you can get some red flags that will help you know that something is amiss, and your credit score is in a danger zone. For instance, when your score is below 600, it is considered a bad credit score. Plus, you can look for ways to boost your score like, contacting companies that help build business credit for employees and businesses in general. Below are some of the signs that will help show you have a bad credit score.

- A loan denial

If you get a loan application denied, it is one of the fast ways and signs that your credit is not in good shape. A good credit score will entitle you to get affordable financing and fast. So, when you apply for a loan, you should get approval with ease. Therefore, when you get turned down for a loan, you can have an idea of where your credit stands. Through this, you can seek ways to improve your business credit and also find ways to get loans and credit to institutions that do not view your credit reports as you figure how to improve your credit score.

- Closed credit card

In such a case where your issuer closes your credit card, it is another sign that you may be having a bad score. This is common as issuers have the habit of reviewing accounts on their own from time to time, particularly in the context of a credit builder card. So, in a case where your score is really low or dropping constantly below the average, they may end up closing your credit card. Also, you may see a change in the terms and conditions of your credit card, specifically related to your credit builder card. For instance, your credit limit decreases. Your credit score may be dropping. Hence, by the time it falls low enough, they then end up closing your account, more so if it has a zero balance.

- A debt collector contacts you

Sometimes a debt collector can contact you, and this is a sign you have a bad credit score, especially in a case where you do not check your credit reports often. Some things that could wind up in collections could be like unpaid utility balances, among other different items. Because of this collections account, they will affect your business and also your personal credit scores. Whereby the companies that own them end up reporting to the credit bureaus. Because of this, get to learn when it is your cue to check your credit. Not only when a debt collector comes calling but when bills start arriving in the mail.

- Having to put a deposit down on a utility account

When seeking to get a utility account for your business and your provider asks you to put a deposit down first. You may have a bad credit score. This is so since it is not only lenders that check through your credit reports, but insurers, utility providers, and cellphone providers as well. It is important for them, as they go through the versions of scores that you have, they can tell whether they should do business with you. For this reason, when you are seeking a utility account, and you have to pay certain fees as a deposit. Your credit score may be poor. So keep this in mind to ensure that you can pick the sign sooner to see how you can improve your score.

- The credit card issuer won't raise your limit

Almost all credit card issuers review your credit when you seek a credit limit raise or a lower annual percentage rate in an existing account. Thus if you happen to get turned down for some reason, it is a sign that your credit report is to blame as there is something that they have seen and have to take that turn of action as they feel uncomfortable having to raise your limit and you are not doing so well on your credit report. So either your business is struggling, or you are mismanaging credit by not paying up, and so your score is going lower.

- You get a default notice

Once you get a default notice or a subpoena from a creditor, your credit report should have sold you out. A default notice is also a way to tell you that you are late on your payments or not making any payments at all. For this reason, they will affect your score negatively. However, by the time they term you as a defaulter, the damage must be big. Similarly, this applies to when they sue you for an old debt. When you are getting the judgment, you are already on the default list.

- You start receiving subprime credit offers

When you start receiving pre-approved offers like secured credit card issuers, car title loan companies, payday lenders from subprime financing providers in your mailbox. This is a possible sign that your credit score has dropped below a certain threshold. Importantly, take note of this if you are more of a person who used to be qualified for prime credit. It should be worrying as credit card solicitations can end up on any mailbox but not subprime credit offers.

In summary, there are many reasons that your credit can be poor. Sometimes you may wonder if there is a mistake or you committed a faux pas that you did not know. Due to this, it is best not to wait for the above signs and get into a habit of checking through your credit report and your credit score to know if you are still in the good range. So thoroughly check your credit to know what might be behind your bad credit.